A data-led read on which luxury houses actually hold value—and why that matters now.

In 2025, luxury’s “big brands” story wasn’t written by runway buzz alone. It was written by price pressure. With global tariff shifts driving up primary-market prices, more buyers treated resale as a smarter point of entry—less about compromise, more about strategy. And in a market where retail keeps climbing, the brands that retain (or exceed) their original value are the ones that set the tone for what “desirability” really means.

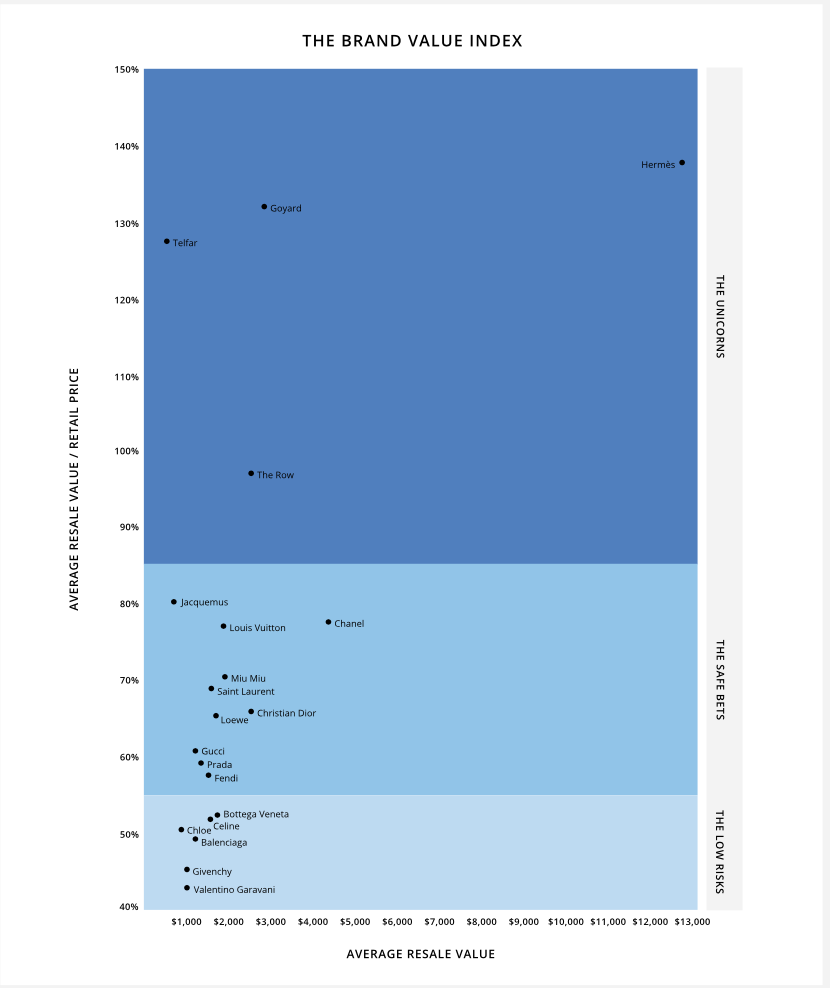

Rebag’s sixth annual Clair Report is built on millions of data points across primary and secondary markets, tracking trends in pricing and demand. Its Brand Value Index maps brands by average resale value and average value retention (resale value vs. retail price), grouping them into three behavioral tiers: The Unicorns, The Safe Bets, and The Low Risks. Think of it as a reality check: not “most talked about,” but “most bankable.”

The 2025 headline: Hermès is back on top

Hermès reclaimed the #1 position this year, returning to dominance in luxury resale with 138% average value retention—a 38% year-over-year increase. That number is more than bragging rights: it signals a brand whose scarcity mechanisms, product codes, and buyer psychology still outperform the inflationary drag hitting most of the category.

In plain terms: Hermès doesn’t merely hold value. It routinely trades above retail—because the secondary market is where access, not just price, gets negotiated.

Why Hermès keeps winning: scarcity, rules, and icons that don’t age

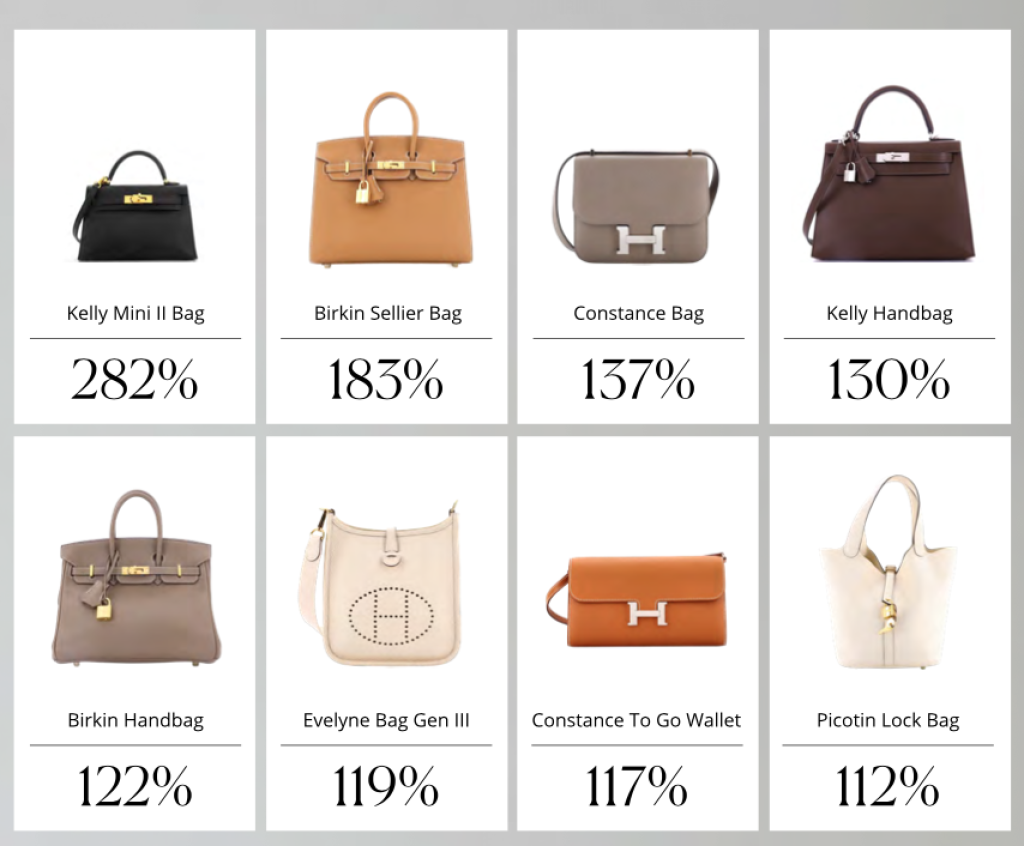

The report is blunt about the mechanics. Hermès dominated the bag category in 2025, with eight styles selling above their original retail value. At the extreme end, the Kelly Mini II led at 282%, followed by the Birkin Sellier at 183% and the Constance at 137%. Even the “core” icons—Kelly, Birkin, Evelyne, Constance To Go, Picotin—cleared 110%+ on average.

And then there are the shopping limits. Rebag points to newly enforced restrictions—two quota bags per year and one registered address per household—as a supply-tightening force that further amplifies secondary-market premiums.

Hermès is no longer a “dream bag” category. It’s a controlled-access market, and resale is where that control turns into measurable price power.

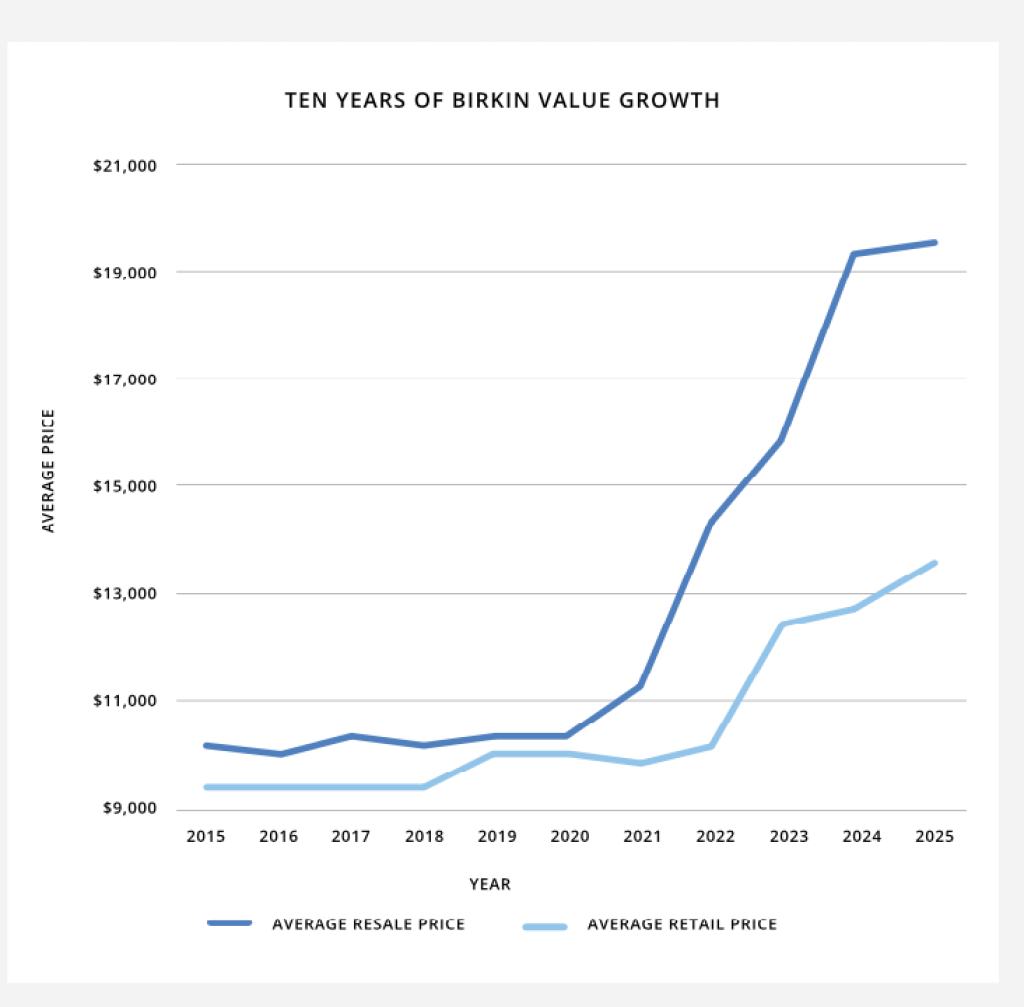

Ten years of Birkin value growth

A decade-long look at Birkin pricing shows sustained appreciation—and a widening gap between retail and resale. Since 2015, average retail prices rose 43%, while average resale values jumped 92%. That spread is the point: secondary-market demand has outpaced Hermès’ own pricing, reinforcing the Birkin’s scarcity and its strength as a collectible asset in the open market.

The market’s confidence was punctuated in July 2025, when the 1984 Jane Birkin prototype sold at Sotheby’s Paris for more than $10 million—a record-setting example of long-term value creation.

Goyard: the quiet powerhouse with loud numbers

Right behind Hermès sits Goyard, posting 132% value retention, up 28% year-over-year. The Brand Value Index visually places it in the top tier alongside Hermès—high retention, high average resale value, and a demand profile that acts more like a club than a conventional brand.

What makes Goyard’s performance especially modern is that it doesn’t rely on constant novelty. It relies on disciplined distribution and controlled availability—then lets the resale market do the marketing.

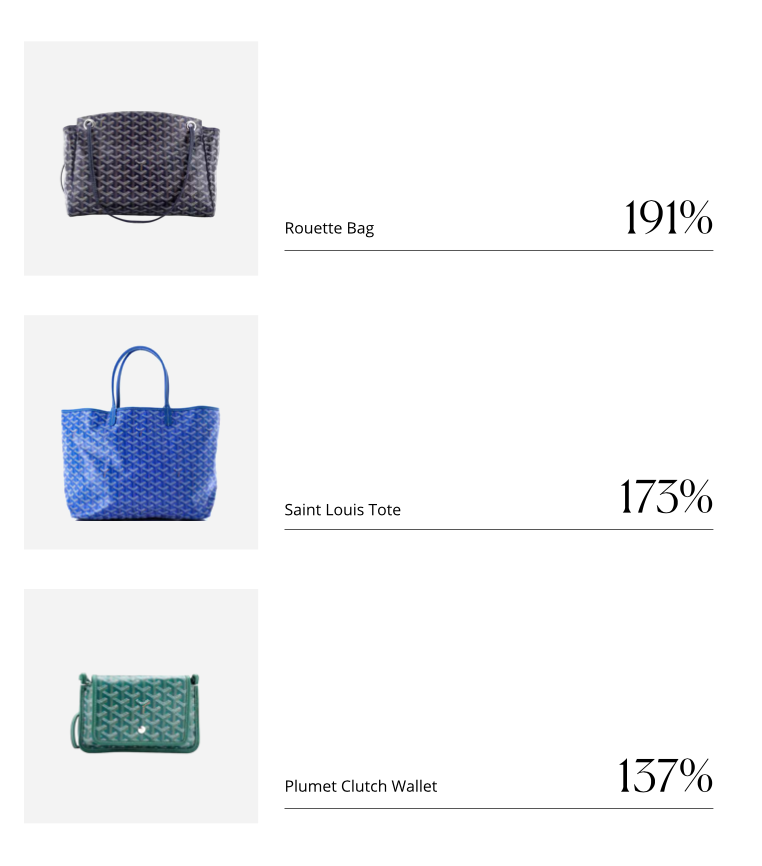

Rebag highlights how “lesser-known designs” are now pulling serious weight, with the Rouette Bag climbing to 191% and the Saint Louis Tote rising to 173%, boosted further by a quiet retail price hike in early 2025.

The Row: officially a “unicorn” brand now

The Row continued its ascent in 2025, with average value retention rising 24% to 97%—a milestone that made it the most culturally telling entry in the Brand Value Index. For the first time, it moved into the report’s “unicorn” category (defined as 85%+ value retention), confirming that the market now treats certain quiet-luxury pieces as genuinely collectible, not just fashionable.

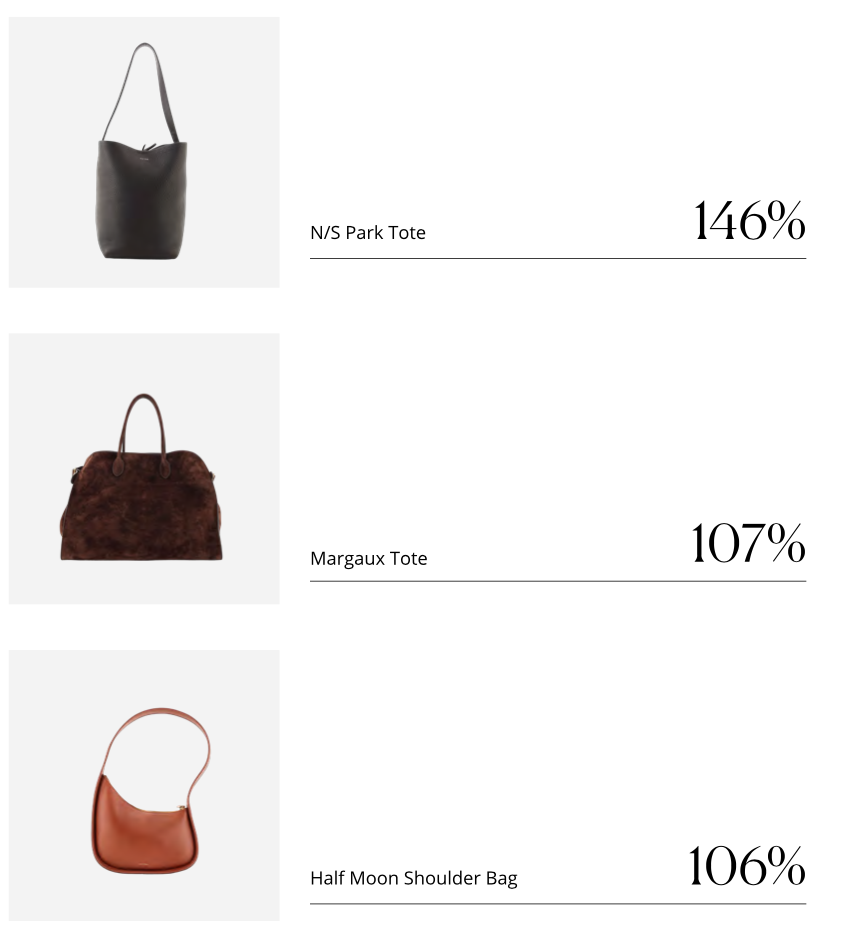

Defined by refined craftsmanship and understated luxury, The Row has become a benchmark for “quiet investment dressing.” Its resale leaders make that clear: the N/S Park Tote topped performance at 146%, followed by the Margaux Tote at 107% and the Half Moon Shoulder Bag at 106%. Together, these numbers reflect a simple shift in buyer behavior: long-term demand is increasingly driven by discreet, logo-free design—powered by consumers who value restraint, material quality, and silhouettes that look expensive in silence, alongside the kind of supply-demand imbalance that turns minimalism into a resale advantage.

The value of Miu Miu

Miu Miu reached new highs in 2025, with average value retention climbing to 104%—its strongest performance to date. What’s notable is that this growth isn’t driven by a single viral moment, but by a tight cluster of styles that the resale market clearly recognizes. The Logo Drawstring Bucket Bag led at 124%, while the Aventure Tote rose to 86% and the Ivy Hobo Bag increased to 83%.

Taken together, these numbers signal an upward trajectory built on Miuccia Prada’s ability to balance youthful energy with enduring sophistication—one of the reasons Rebag positions Miu Miu as one of the most compelling “investment” names in contemporary luxury right now.

What the rest of the index is really saying

Beyond the top three, the index becomes a map of buyer behavior:

The Unicorns are where resale acts like a parallel retail channel—often above retail, often hard to get, and culturally resilient. The chart places Hermès, Goyard, The Row, and Telfar in this top tier.

The Safe Bets are brands people buy with confidence because demand is broad and liquidity is high. In the chart, this zone includes names like Chanel, Louis Vuitton, Jacquemus, Miu Miu, Saint Laurent, Dior, Loewe—the brands that move volume and remain easy to resell, even when they don’t beat retail.

The Low Risks zone contains brands that still resell—but with less price insulation. The chart clusters Bottega Veneta, Celine, Chloé, Balenciaga, Valentino Garavani, Givenchy and others lower on the retention axis. The message isn’t “don’t buy.” It’s “buy because you love it, not because you expect it to behave like an asset.”

How to use this as a shopper (and as a closet strategy)

If you’re buying with resale in mind—or you simply want your wardrobe to age well—the 2025 Brand Value Index suggests three practical rules:

First, prioritize constrained access (true or engineered). Hermès and Goyard don’t “perform” because they’re prettier. They perform because supply is rationed and distribution is controlled, which pushes price discovery into the resale market.

Second, buy the style that the market already recognizes. For Hermès, Rebag’s own style-level data shows that the market pays the biggest premiums for pieces like Kelly Mini II, Birkin Sellier, and Constance. For The Row, the demand concentrates around a small set of silhouettes (Park, Margaux, Half Moon).

Third, treat care and storage as value protection—not as a nice-to-have. The resale market rewards structure, shape, corners, and overall “kept” condition. (If you want a clean, brand-aligned soft CTA for LaForma: this is where you naturally mention that a well-fitted pillow insert helps maintain silhouette and reduce creasing—especially for softer leathers and unlined shapes.)

The 2025 takeaway in one line

2025 wasn’t just a year of “it bags.” It was a year where the market clarified which brands are culture-proof and price-proof—and it put Hermès, Goyard, and The Row at the center of that story.