Dior and Chanel bags under €4,000 are suddenly the most telling signal in luxury’s current mood swing: not a retreat from prestige, but a redesign of the ladder that gets shoppers back into the brand before they disappear into resale—or into nothing at all. The premise is simple. After several years of price-led growth, the fastest route to stabilising demand is making sure there are still reasons to buy that don’t start at five figures.

Dior and Chanel bags under €4,000: what’s changing (and how fast)

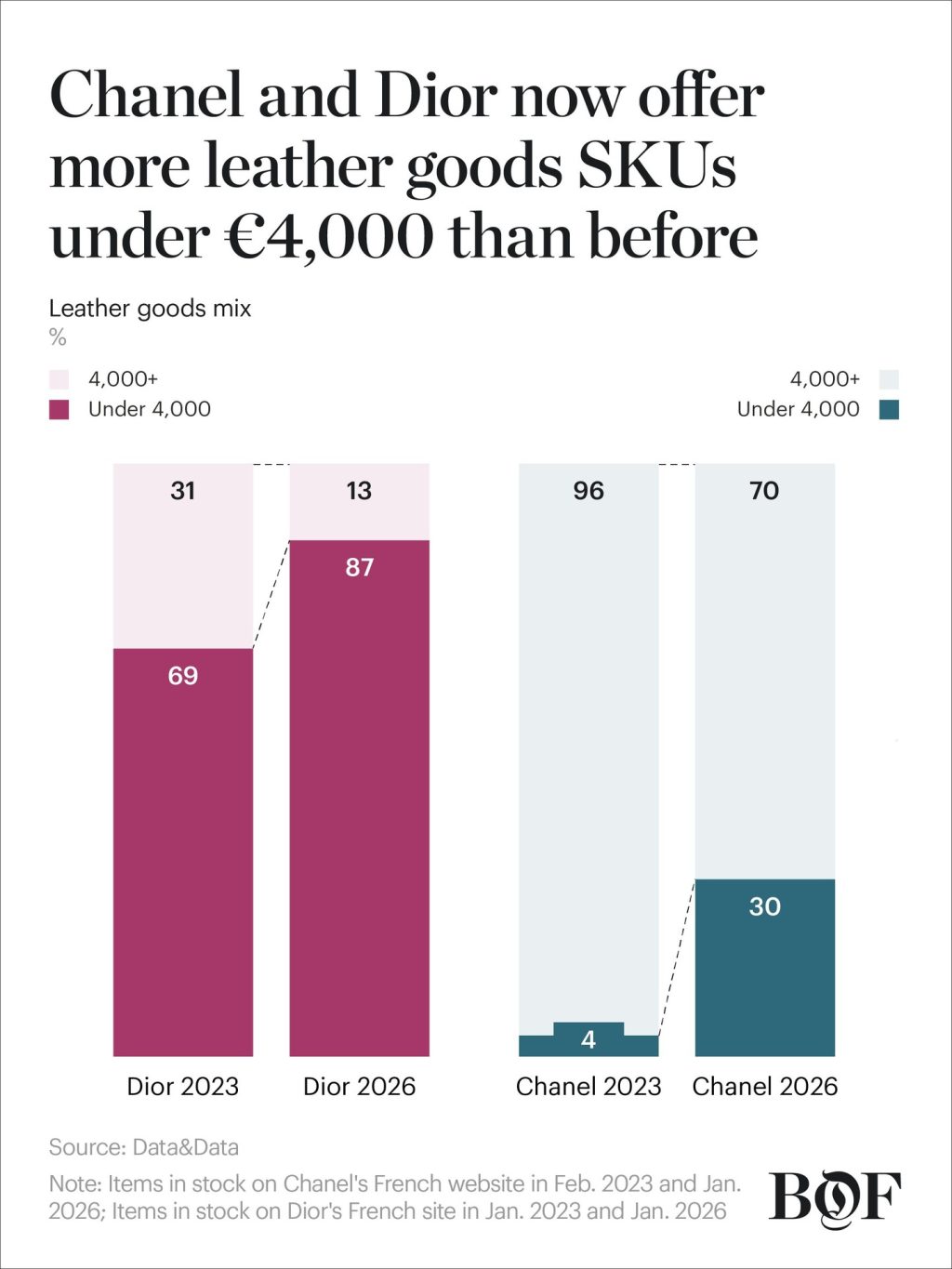

The bluntest proof point sits inside the leather-goods assortment mix. In a BoF-published graphic (stocked items on the brands’ French sites), Dior’s leather goods under €4,000 rise from 69% (Jan 2023) to 87% (Jan 2026). Chanel moves from 4% (Feb 2023) to 30% (Jan 2026) under the same €4,000 threshold. Dior’s swing is acceleration; Chanel’s is a philosophical pivot, because it starts from near-zero “buy-in” territory.

That distinction matters. Dior already had an entry ladder inside leather goods—more wallets, smaller formats, and seasonal bags playing in the “reachable” zone. Chanel, historically, behaved as if leather goods should train you upward, fast. Now it’s widening the base, even while the top stays protected.

The leather-goods mix: Dior vs Chanel, 2023 to 2026

This is where the €4,000 number becomes a strategy shorthand, not a consumer promise. It doesn’t mean “more cheap handbags.” It means more SKUs that keep leather goods culturally present—charms, SLGs, small accessories, and a few handbag silhouettes that don’t immediately trip into the €4,500–€6,000 band.

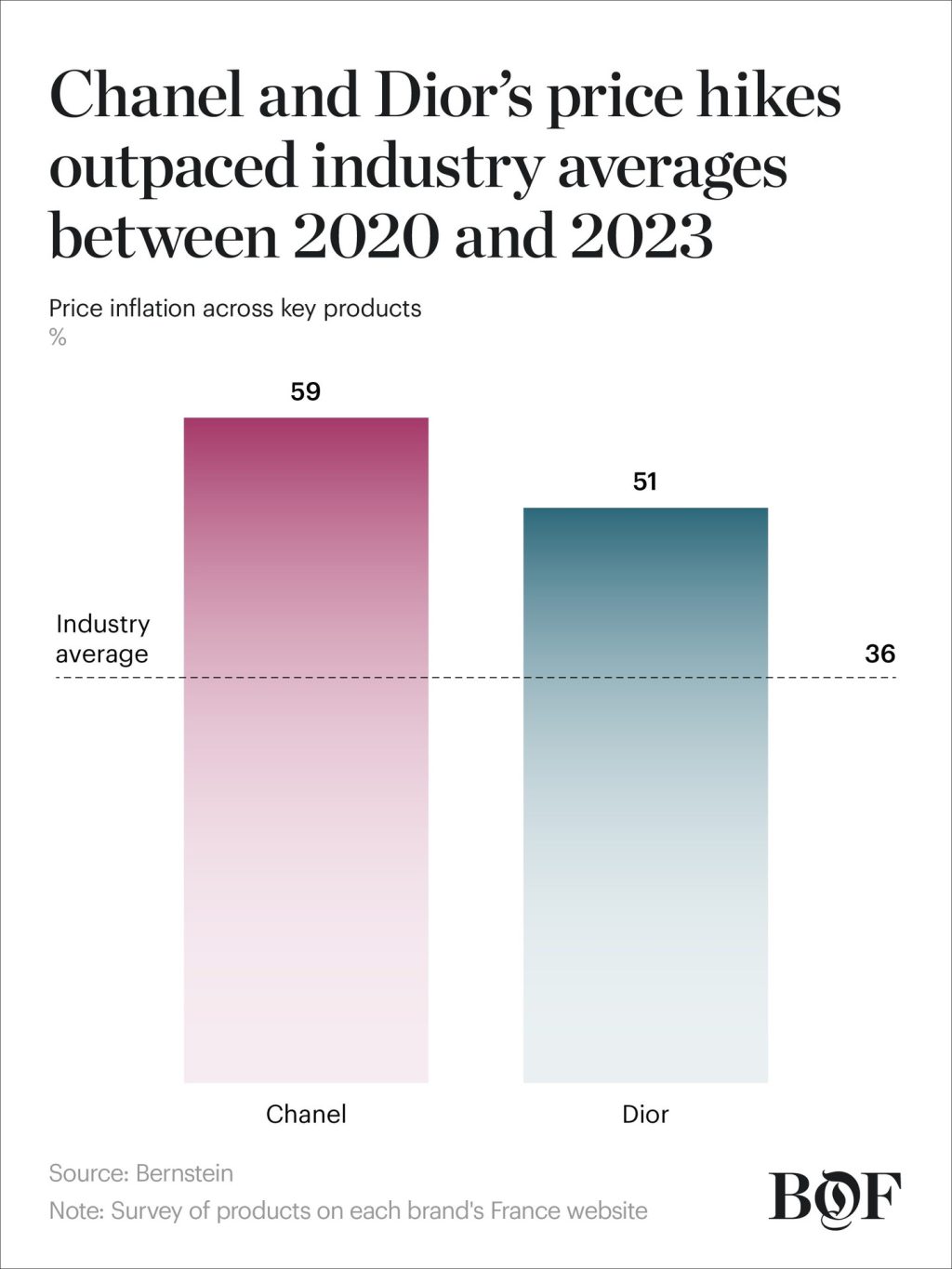

Why luxury can’t “grow through price” forever

Luxury spent the post-pandemic boom years raising prices faster than it refreshed product. McKinsey notes that, in the recent expansion cycle, price increases accounted for a dominant share of growth, while volume gains were comparatively modest.

The reset is now visible in the demand base. Bain/Altagamma reports that the global luxury consumer pool is shrinking from about 400 million (2022) to ~340 million (2025)—a dramatic reversal for an industry that treated “elevation” as a one-way escalator.

At the same time, the rest of the market is leaning harder on promotions: the Financial Times reported that up to 40% of luxury goods were sold at a discount in 2025, a level that signals pressure on both inventory and perceived value.

So the 2026 problem isn’t only macro. It’s behavioural: shoppers have learned to wait, compare, and sanity-check price against resale. In that environment, rebuilding volume doesn’t mean slashing icons. It means designing a credible “yes” below the psychological pain point—and doing it in categories that still feel like the brand.

And the access conversation isn’t limited to price—see Hermès client profiling allegations: what’s being claimed—and what can be proven for how “who gets to buy” has become part of the luxury debate.

The €4,000 line: what it actually buys you

€4,000 is less a number than a threshold of justification. Above it, shoppers demand permanence: leather quality, hardware integrity, silhouette longevity, repairability, and resale logic. Below it, they will tolerate more “fashion”—as long as it still reads like the house.

That’s why the under €4,000 expansion skews toward:

- Small leather goods (wallets, small crossbodies, compact totes)

- Fashion jewellery (earrings, bracelets, charms)

- Accessories that live close to the face (scarves, headbands)

- Seasonal handbags that can carry a trend without threatening the icon hierarchy

Done well, it’s not dilution. It’s reacquisition.

Dior’s renewed pricing architecture: a pyramid with more footholds

The Dior pyramid in the BoF graphics makes the intention legible: the base is wide, the middle is active, the top is aspirational.

At the apex sits a Small Lady Dior Shoulder at €9,400; the “core” Lady Dior anchors at €6,200. The message is classic luxury: the icon remains the icon.

For runway context behind Dior’s object decisions, our Dior Haute Couture Spring–Summer 2026 bags guide decodes the silhouettes driving desire at the top of the pyramid.

The €3,000–€4,700 band: where handbags behave like “entry” again

This is Dior’s conversion zone. In the snapshot: a Small Bow Bag at €3,700; a Lady D-Joy Mini Dioramour at €4,650; even ready-to-wear (a Dioamour cardigan at €3,200) is placed in the same “reachable luxury” band. It’s a curated argument that you can buy into the Dior universe without immediately crossing into core-bag money.

The subtle shift is psychological. The customer isn’t being asked to save for Dior. She’s being given permission to start with Dior.

The ladder-building isn’t only womenswear—Dior Fall/Winter 2026 menswear bags guide tracks the same object-led strategy through a different wardrobe.

The sub-€1,500 band: the souvenir economy (charms, earrings, scarves)

Below €600, the pyramid becomes a brand-intimacy shelf: earrings (€460), bracelet (€480), bag charm (€500), scarf (€520). Those numbers are not accidental. They’re engineered to create repeatable gifting, impulse purchase, and “first Dior” moments—especially when a €6,200 bag feels like a thesis defence.

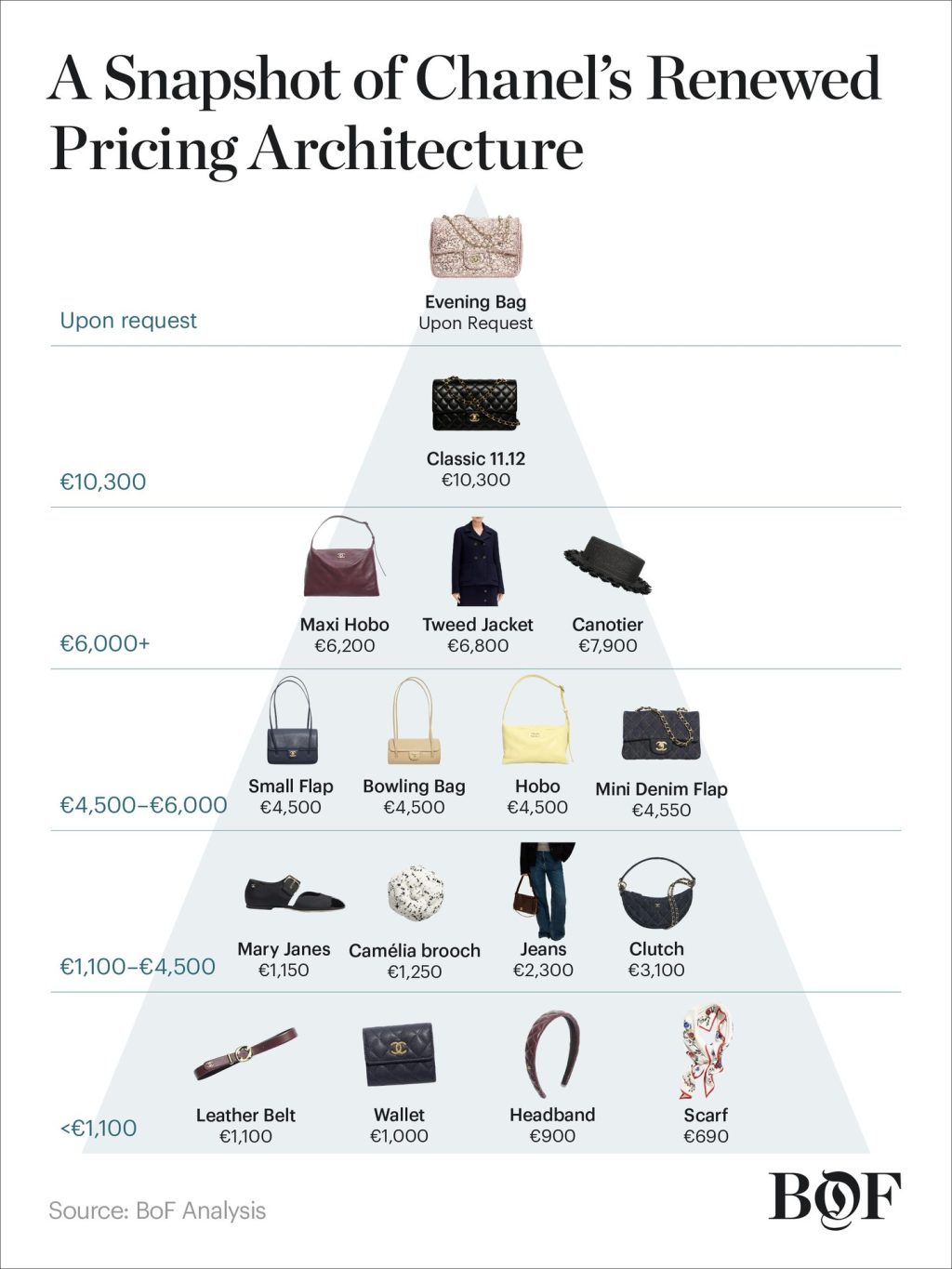

Chanel’s renewed pricing architecture: protect the icon, widen the base

Chanel’s pyramid is colder—and that’s the point. The icon is the ice wall.

The snapshot places the Classic 11.12 at €10,300, with an “upon request” evening bag above it. This is Chanel reminding you that its centre of gravity is still the classic flap mythology.

For the clearest read on Chanel’s top-of-pyramid storytelling, see our Chanel Spring–Summer 2026 Couture Bags—where the house turns mythology into objects.

The €4,500–€6,000 wall: Chanel’s strategic choke point

Chanel’s notable band is the one just above the €4,000 headline. The pyramid shows multiple handbags sitting at €4,500 (Small Flap, Bowling Bag, Hobo) and a Mini Denim Flap at €4,550—a tight cluster that reads like a deliberate threshold. You can step into a Chanel bag, but you do so above €4,000.

So how does Chanel expand “under €4,000” in leather goods? It does it with everything adjacent to the bag.

Under €1,100: the accessories base that keeps the brand “buyable”

The base tier is packed with items designed to keep Chanel in reach: wallet (€1,000), headband (€900), scarf (€690), leather belt (€1,100). These are daily-wear touchpoints—products that keep the brand in your life even when the icon bag is postponed.

That’s the new logic: frequency at the base, aspiration at the top.

Materials, construction, and value density: what to look for under €4,000

If you’re shopping the under €4,000 zone, think in “value density,” not logo density.

Prioritise:

- Full-grain leathers and clean edge finishing (look for crisp glazing and consistent paint lines)

- Hardware weight and plating consistency (cheap hardware ages loudly)

- Strap comfort + attachment engineering (stress points reveal cost-cutting fastest)

- Silhouette structure (a bag that collapses early feels overpriced)

Be stricter with “small.” SLGs can be wonderful, but flimsy interiors and weak snap closures are where luxury sometimes quietly economises.

Buying guide: how to shop the under €4,000 zone like a collector

Use this checklist before you buy:

- Decide the job: everyday, occasion, travel, or “brand token”?

- Measure the wear: cost-per-wear beats price; don’t buy “special” and never use it.

- Audit the closure: zips, magnets, turn-locks—test them like you’re buying luggage.

- Check the corners: structure + abrasion tells you the truth about longevity.

- Think storage now: structured bags keep value when they keep shape.

A practical note from the bag-care side: if you’re buying smaller leather goods or seasonal handbags as your “entry,” preserve them like future heirlooms. Using bag pillows to support structure (especially for softer leathers and compact formats) helps prevent sagging and corner collapse—the kind of wear that quietly erodes resale value over time. A well-kept piece doesn’t just photograph better; it ages with intent.

Alternatives: resale, vintage, and “value luxury” as the shadow competition

Here’s the part brands can’t say out loud: the toughest competitor is the product they already sold.

The secondhand market has become a parallel pricing engine. BCG and Vestiaire Collective highlight secondhand’s rapid growth trajectory and how embedded resale has become in real wardrobes.

Meanwhile, The RealReal’s reporting culture (and the broader coverage around it) keeps reminding shoppers to compare “new” with “pre-owned” before paying full retail—especially for brands where classics anchor value.

That’s why Dior and Chanel expanding under €4,000 matters: it’s a way to compete with resale without becoming resale. Not through discounting, but through new, brand-controlled entry points that keep customers inside the boutique ecosystem.

***

Dior and Chanel aren’t abandoning elevation—they’re correcting its blind spot. When luxury’s growth can’t rely on price alone, the winning move is rebuilding a believable ladder: small, beautiful, wearable entry points that keep the brand in circulation until the shopper is ready to trade up. For collectors, the opportunity is clarity: buy the tier that fits your life, then preserve it like it already belongs to your archive.